If you're looking into braces for yourself or your child, the first question often isn't about brackets or aligners. It's about the monthly payment. Families across Santa Ana, Costa Mesa, Tustin, Irvine, and Garden Grove often reach the same moment: you want to move forward, but you also need the cost to fit into real life.

That concern is reasonable. Orthodontic treatment is a health decision, a confidence decision, and a budgeting decision all at once. Those seeking treatment aren't trying to become financing experts. They just want a clear explanation of what they'll owe, when they'll owe it, and what questions to ask before signing anything.

This guide is written to make that part easier. If you're balancing treatment with groceries, school costs, rent, or other care like Invisalign, dental implants, sleep apnea treatment, cosmetic dentistry, or emergency dentistry, understanding the structure behind braces monthly payments can help you plan with less stress. Every article for Bristol Dental & Orthodontics is reviewed by Dr. Andrew Finley before publishing.

Table of Contents

- Making a Straighter Smile Fit Your Budget

- How Orthodontic Monthly Payments Are Calculated

- Your Payment and Financing Options in Orange County

- Example Monthly Payment Scenarios

- Tips for Making Orthodontic Treatment More Affordable

- Schedule Your Personal Financial Consultation in Santa Ana

Making a Straighter Smile Fit Your Budget

A lot of orthodontic decisions start at the kitchen table.

A parent in Orange County notices their child covering their smile in photos. An adult who missed braces as a teen finally feels ready to ask about treatment. Someone else has already been comparing options online and keeps circling back to one concern: "Can we afford the monthly payments?"

That question deserves a calm answer, not pressure.

For many families, the challenge isn't whether treatment matters. It's figuring out how to fit it into everything else already competing for the monthly budget. One household may be planning around after-school activities. Another may be handling commuting costs between Santa Ana and Irvine. Someone else may be trying to leave room for future care, like cosmetic work or replacing a missing tooth with an implant.

A good financial conversation should leave you feeling informed, not cornered.

Braces monthly payments usually become less intimidating once you understand how they're built. The payment you see on paper didn't appear out of nowhere. It's based on a few moving parts that can often be discussed and adjusted during a consultation.

If you're organizing expenses before that appointment, it can help to review a practical household planning resource like Koru's guide to family budgeting. Not because orthodontic care is the same as any other bill, but because a clearer family budget makes treatment decisions feel more manageable.

Three ideas help most readers right away:

- Monthly payments are usually structured, not random. Practices typically start with the treatment fee, then look at the upfront amount and the payment timeline.

- The lowest upfront amount isn't always the best fit. Some families prefer a smaller start and higher monthly amount. Others do the opposite.

- The contract matters as much as the payment. A manageable monthly number still needs to come with clear terms.

That last point is where people often get surprised. They focus on the monthly figure and forget to ask what happens if life changes. We'll get into that in plain language.

How Orthodontic Monthly Payments Are Calculated

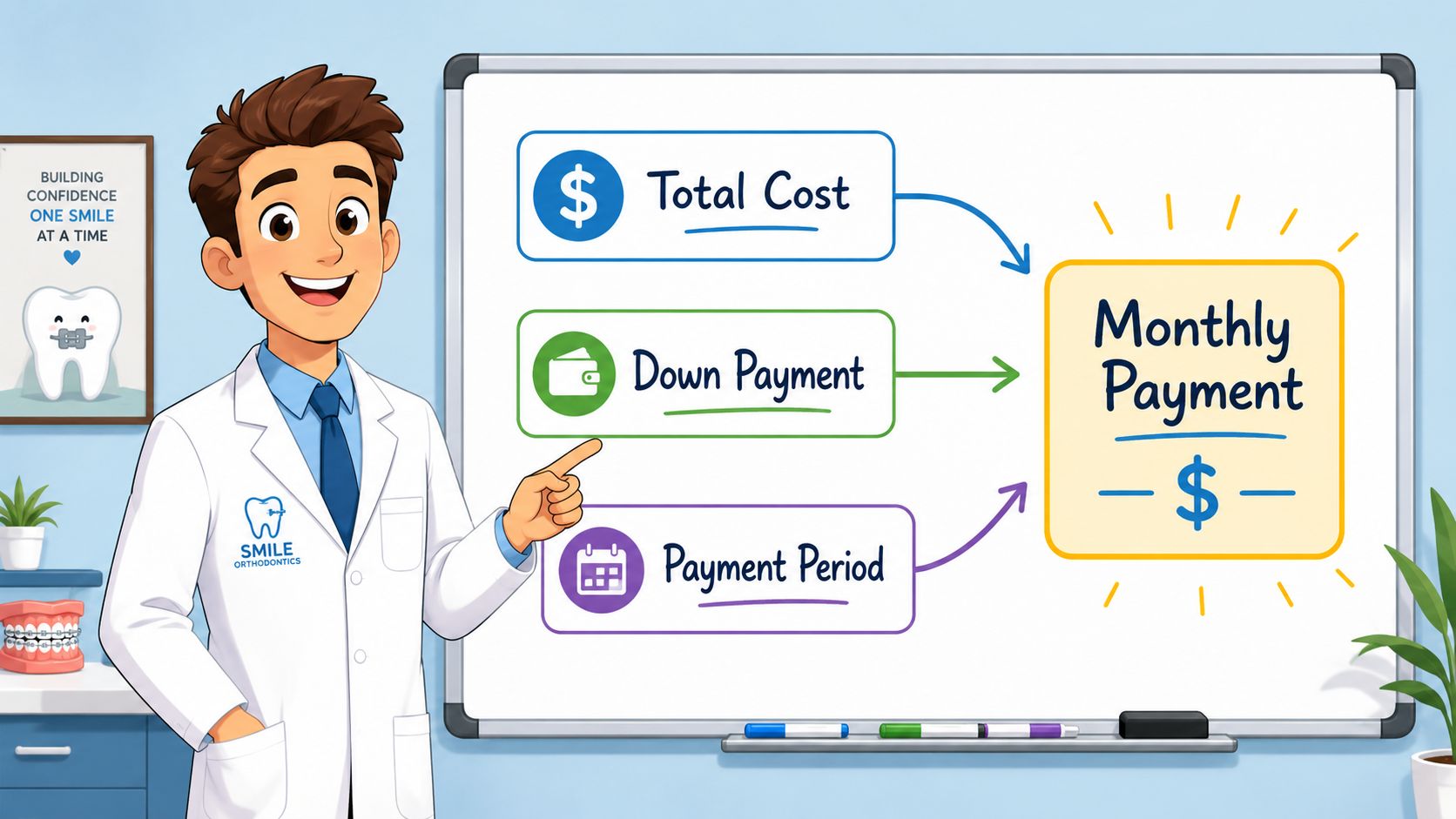

The easiest way to understand braces monthly payments is to think of them like a home project. First there's the full project cost. Then you decide how much you want to put down at the beginning. After that, the remaining balance gets spread over time.

Here's the visual version.

The three pieces that shape the payment

Most orthodontic payment plans come down to three parts:

The total treatment fee

This reflects the type of treatment and the complexity of the case.The down payment

This is the amount paid upfront before the remaining balance is divided into monthly installments.The payment term

This is the number of months used to spread out the remaining balance.

The simplest formula looks like this:

Total fee minus down payment, divided by the term, equals the monthly payment.

That doesn't mean every office uses the exact same policies. It does mean the structure is usually easier to understand than many patients expect.

What 0 percent financing usually means

One of the biggest worries patients bring into a consultation is interest. That's why it helps to know that the standard industry practice is to offer 0% interest monthly plans, allowing patients to pay the full principal without finance charges. One example from this orthodontic payment plan explanation shows a typical structure where a $5,000 balance after a $1,000 down payment on a $6,000 fee is spread across 24 months, resulting in a monthly payment of about $208.

That example isn't a quote for any one patient in Santa Ana. It's a simple way to see the math.

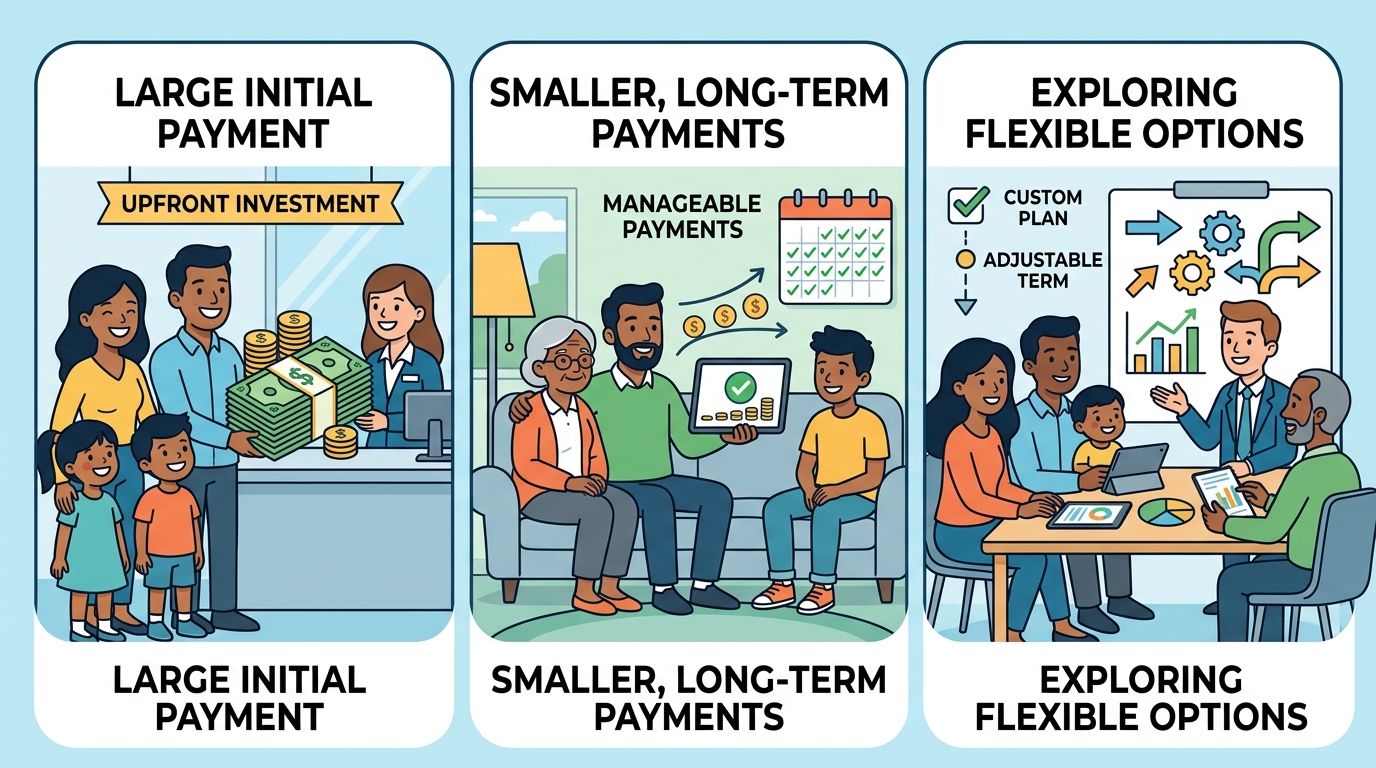

Practical rule: If you want a lower monthly payment, ask whether changing the down payment or extending the term would help.

Sometimes a family can put more down at the start and bring the monthly amount down. Sometimes preserving cash upfront is more important, so they choose a smaller initial payment and accept a higher monthly figure. Neither approach is automatically right. The better fit depends on your household.

Why offices structure plans this way

Orthodontic plans are often designed around what people can realistically budget month to month. That makes the payment conversation less about abstract finance and more about timing and predictability.

From the practice side, this kind of structure also helps administrative teams keep accounts organized. If you're curious how benefits and billing details can affect payment coordination behind the scenes, optimizing medical billing cash flow offers useful background on why clean payment systems matter.

A few good questions can make the math clearer fast:

- What is included in the quoted treatment fee

- How much is due upfront

- How long does the payment plan last

- Is the plan interest-free

- Can I change the payment structure if needed before treatment starts

Those questions help you compare options without feeling like you're decoding fine print.

Your Payment and Financing Options in Orange County

A parent in Santa Ana might walk into a consultation thinking the big question is, "What do braces cost per month?" A more useful question is, "Which payment pieces can we combine to make this workable for our family?"

That shift matters. In Orange County, orthodontic financing often works like building a monthly plan from a few parts: office payments, insurance benefits, and sometimes HSA or FSA funds. The goal is not just a number that fits today. It is an arrangement you still feel comfortable with if treatment lasts many months and life gets busy.

Comparing Your Orthodontic Payment Options

| Option | How It Works | Best For Patients Who… |

|---|---|---|

| In-house payment plans | The office divides treatment costs into scheduled payments, often with straightforward terms | Want a simpler, office-based arrangement |

| Third-party financing | A separate financing company handles approval and repayment terms | Want another route when office terms don't fit |

| Dental insurance | Insurance may pay part of eligible orthodontic treatment, reducing what you finance | Already have orthodontic benefits to apply |

| HSA and FSA funds | Tax-advantaged healthcare dollars can be used for eligible treatment expenses | Want to use set-aside healthcare funds strategically |

In-house payment plans

For many families, in-house plans feel easiest to follow because the payment discussion stays with the same team handling treatment. That can make a confusing subject feel more manageable.

It works a bit like setting up a household bill with one office instead of splitting questions across several companies. You can ask how often payments are due, whether automatic payments are available, and what happens if you need to adjust timing before treatment begins.

This is also the point where contract details matter. Ask what the total fee includes, whether retainers or repairs are separate, and what happens if treatment is discontinued early. A discontinuation policy tells you how charges are handled if a patient stops treatment before the original end date. Families often miss that line, then wish they had asked sooner.

Patients often prefer in-house plans when they want:

- One clear point of contact

- Straightforward due dates

- An easier way to ask billing questions during treatment

- A chance to review office policies before signing

Third-party financing

Outside financing gives some patients another option when the office's standard structure does not fit their budget. The monthly payment may look appealing at first glance, but the contract deserves the same attention as the number.

A good comparison is a cell phone plan. The monthly charge matters, but so do the terms behind it. Orthodontic financing works the same way.

Ask about:

- Approval requirements

- Interest or fees

- What happens after any promotional period

- Whether you can pay early without penalty

- How missed payments are handled

- What happens if treatment stops unexpectedly

A lower monthly payment can still be a poor fit if the agreement becomes expensive or hard to manage later.

Dental insurance

Insurance can lower what you owe, but each plan has its own rules. Understanding insurance details helps you ask better questions during your consultation.

Private dental plans may include orthodontic benefits with age limits, lifetime maximums, or waiting periods. Public coverage can follow stricter medical-necessity rules for children and may not cover adult orthodontic treatment, as explained in this discussion of braces coverage and payment questions.

That is why two Orange County families with "insurance" may end up with very different out-of-pocket costs.

A helpful way to approach this is to ask the office to break insurance into three plain-language pieces:

- What your plan may pay

- What amount would still be yours

- When insurance payments and your payments are expected

That kind of conversation gives you a clearer map before treatment starts.

HSA and FSA funds

HSA and FSA accounts can ease pressure on your regular monthly budget because they let you use healthcare funds you already set aside. Families sometimes overlook this option until they are close to signing paperwork.

These accounts usually work best as part of a larger plan, not as a stand-alone answer. For example, a patient might use insurance first, apply HSA or FSA dollars to eligible costs, and then place the remaining balance on an in-house payment schedule.

Before using HSA or FSA funds, ask:

- Whether your planned treatment qualifies

- What receipts or documents you should keep

- Whether reimbursement timing matters

- How those funds can be combined with your other payment arrangements

A clear financing plan should feel understandable on paper and realistic at home. If a quote looks good but the rules around it feel fuzzy, that is a sign to slow down and ask more questions.

Example Monthly Payment Scenarios

Real life rarely looks like a perfect financing worksheet. Most households combine a few strategies based on timing, benefits, and what else is happening that year.

A family planning around school expenses

A Santa Ana family wants braces for their teenager, but the timing lands right between school costs and holiday spending. They don't want to delay treatment longer than necessary, yet they also don't want a payment that feels tight every month.

So they ask a practical question: would a larger upfront payment create a more comfortable monthly amount?

That doesn't change the fact that treatment still needs to be paid for. It changes the shape of the obligation. For many families, that structure works better than trying to minimize the start and then feeling stretched later.

An adult choosing Invisalign

An adult in Irvine wants a more discreet option because of work meetings and social comfort. They ask about Invisalign and how payments compare with more traditional orthodontic treatment.

For many patients, Invisalign treatment takes between 6 and 18 months, according to this overview of Invisalign timelines. That timeline often fits naturally with many orthodontic payment arrangements. Instead of treating the financial plan and the treatment plan as separate topics, patients can discuss them together.

This example matters because adults often assume they have only two choices: pay a large amount upfront or postpone treatment. In many cases, there are more flexible ways to approach it.

Some patients do best when they match the payment schedule to the expected treatment timeline instead of treating financing as an afterthought.

A patient preparing for more than one dental priority

A patient in Garden Grove isn't only thinking about straightening teeth. They may also need future cosmetic care, may be evaluating a missing tooth, or may want to address sleep-related symptoms with an oral appliance after speaking with a dentist.

That kind of patient benefits from stepping back and looking at the whole care picture. Orthodontic treatment doesn't happen in a vacuum. If you expect additional dental work later, preserving some flexibility in your payment structure can matter as much as the monthly amount itself.

A few planning habits help in cases like this:

- Map the order of care so you know what likely comes first

- Ask which services are separate from the orthodontic agreement

- Leave room in your budget for unexpected dental needs

- Review timing carefully if you may start more than one type of treatment in the same year

These scenarios aren't promises about what any one patient will pay. They're examples of how families and adults often think through braces monthly payments in everyday life.

Tips for Making Orthodontic Treatment More Affordable

Affordability isn't only about finding the lowest number. It's about building a plan you can stick with. A payment that looks good on day one can still cause stress later if the terms are unclear or the timeline doesn't fit your life.

Questions worth asking before you sign

One of the most important parts of an orthodontic consultation happens after the clinical discussion. That's when you ask the questions many patients forget until it's too late.

The American Association of Orthodontists notes that life can change unexpectedly, and its guidance on payment plans and financial hardship reminds patients to ask about treatment cancellation policies, hardship situations, and whether contracts may include penalties or balance acceleration clauses.

Ask these directly:

- If treatment stops early, what happens to the remaining balance

- Are any fees non-refundable

- If my financial situation changes, is there a hardship process

- Can the payment date be adjusted

- Does the agreement allow early payoff without penalties

Those questions can feel uncomfortable. Ask them anyway. Clear answers protect you.

Simple ways to reduce financial stress

Patients often have more room to plan than they think. The best approach is usually a combination of timing, organization, and clear communication.

Consider these habits:

- Use consultation time wisely. Bring your insurance information, HSA or FSA details, and your main budget concerns so the office can explain options in one conversation.

- Think in total budget terms. Don't focus only on the monthly number. Look at the full agreement, including what is and isn't included.

- Ask about treatment type differences. Traditional braces, ceramic braces, and Invisalign may involve different financial structures depending on your case.

- Plan around known expenses. If you already know when tuition, travel, or holiday costs spike, say so before the payment plan is finalized.

Ask this out loud: "If my life changes during treatment, what flexibility do I have?"

That single question can reveal whether a plan is built for real life or only for ideal circumstances.

Another useful step is to think ahead if orthodontics isn't your only dental goal. Adults sometimes start with alignment, then want whitening, bonding, veneers, implants, or sleep apnea appliance therapy later. If that sounds like you, don't treat each decision as isolated. A more balanced approach can help you avoid overcommitting too soon.

Schedule Your Personal Financial Consultation in Santa Ana

A consultation often feels more manageable once you know what questions to bring. Instead of hearing one monthly number and hoping it works, you can ask how the plan is built. That includes the total fee, any down payment, insurance timing, HSA or FSA use, and what happens if treatment pauses or ends early.

For many Santa Ana families, that is the turning point. The conversation shifts from "Can we afford braces?" to "Which payment structure fits our household best?"

Here is the practice website preview.

Before your visit, it helps to gather the same details you would want before starting any long-term family plan. Bring your insurance card, a list of medications, your main budget concerns, and a few direct questions about contract terms. If you like to organize things ahead of time, Formzz patient intake templates can help you map out what information to collect before you come in.

A personal consultation also gives you context that an online estimate cannot give. Your treatment recommendation depends on your teeth, your bite, your goals, and how long care is expected to last. The financial side should match that reality. A clear conversation can show whether payments are spread evenly, whether insurance is applied up front or over time, and whether the office offers flexibility if your circumstances change.

That matters for parents planning care for a child, adults comparing braces with clear aligner treatment, and patients trying to balance orthodontics with other dental needs.

If you are ready to sit down with someone who can explain the numbers in plain language, Bristol Dental and Orthodontics welcomes you to schedule a consultation. Dr. Andrew Finley and the team can review your treatment options, answer questions about how payment plans are structured, and help you understand what to look for before you agree to a financial plan.